{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

The EU is increasing the level of transparency another notch in order to detect potentially aggressive tax arrangements. We help you meet DAC6’s massively tightened disclosure rules.

The EU is introducing an additional level of transparency in order to detect potentially aggressive tax arrangements.

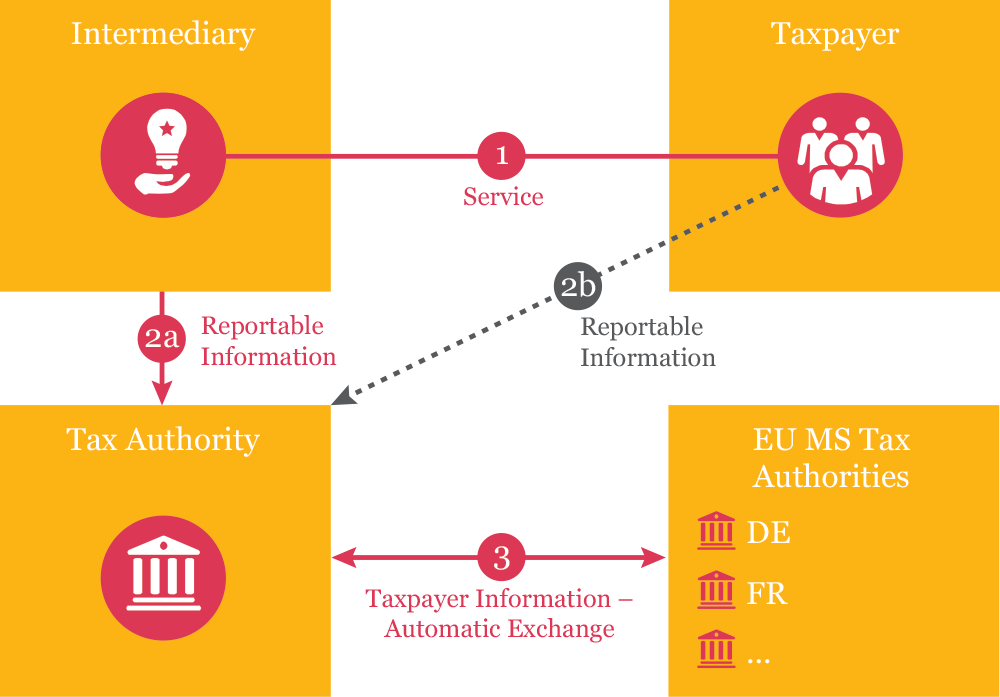

The amendment to Directive 2011/16/EU on mandatory automatic exchange of information in the field of taxation in relation to reportable cross-border arrangements (DAC6 for short) will have far-reaching consequences for tax advisors, service providers and taxpayers – including organisations and individuals in Switzerland and Lichtenstein.

DAC6 imposes mandatory disclosure requirements for certain arrangements with an EU cross-border element where the arrangements fall within certain "hallmarks" mentioned in the directive and in certain instances where the main or expected benefit of the arrangement is a tax advantage. There will be a mandatory automatic exchange of information on such reportable cross-border schemes via the Common Communication Network (CCN) which will be set-up by the EU.

Become DAC6 compliant with our tool

The recent decision by the European Commission to amend the Directive on administrative cooperation (DAC6) to allow for an optional six month deferral of reporting deadlines has had a major impact on the DAC6 projects of multinational groups. The revised reporting deadlines for those countries where the deferral applies are as follows:

Although the adoption of the deferral has been official announced or is expected to be announced by the vast majority of the Member States, there have been three countries where no deferral has been provided for.

Austria, Finland, and Germany have announced that the deadlines for reporting would still apply as per the original DAC6 deadlines. Please note that reporting in Austria is not possible for IT reasons and a 'de facto' deferral is applied. A three-month deferral effectively applies for new arrangements and a two-month deferral for legacy arrangements (and thus no penalties would apply for late filing up to that time).

On 31 December 2020, the UK Government announced that the scope of reporting under DAC6 would be limited to cross-border arrangements under the category D hallmarks (which relate to CRS avoidance and opaque ownership structures). Intermediaries and relevant taxpayers in the UK will not need to report arrangements under hallmark categories A, B, C and E (unless category D was also met).

Individual Member States are issuing local guidance and reporting information on a regular basis. As DAC6 is officially live, there is no time to lose in preparing for this regulation. We can help you cover all the bases:

Get in touch with us. We’ll help you rapidly work out where you stand and make the necessary preparations, expertly and efficiently.

{{item.text}}

{{item.text}}