Benjamin Rutz

Director, Business Restructuring Services, PwC Switzerland

Claude Fuhrer

Partner, Deals Strategy & Operations Leader, PwC Switzerland

In this blogpost we paint in broad strokes recent developments in industrial manufacturing, including the Swiss sector. Areas of concern: input costs, gas supply, cash flow and value preservation.

Input costs and impending energy shortages

Industrial manufacturers are major consumers of energy and raw materials. Many have been hit hard by higher energy prices and commodity market volatility, as well as having to contend with supply chain issues and substantial increases in other input costs such as labour.

The impact of higher energy prices varies depending on how effectively hedged a company is and the extent to which it can pass costs on to customers. Even companies currently able to do so could face tighter working capital requirements once price arrangements in energy contracts expire, as some energy suppliers will only be renewing subject to shorter payment terms or upfront deposits. They may also reach the point where demand is no longer elastic, forcing them to look for other ways of improving margins to compensate for rising costs.

With production costs threatening to become untenable, some manufacturers are planning for shutdowns in production over the winter. Another factor increasing the risk that heavy industry may also have to be shut down is the real threat that the gas supply will be interrupted.

“With input price inflation and the risk of production shutdowns piling on the pressure, industrial manufacturers are vulnerable at the moment. This could create potential for deals as they review portfolios and divest core assets.”

Mixed signals from the industry

There have been some rays of hope, however. The fact that second-quarter industrial production in the euro area exceeded expectations suggests than supply chain problems have eased, enabling companies to process existing orders more quickly. On the other hand, August saw a further decline in the manufacturing Purchasing Managers’ Index (PMI) as manufacturers reined in their buying activity in anticipation of a deterioration in the economy.

Euro Area Manufacturing Purchasing Managers’ Index (PMI)

Source: Markit Economics

Strategic responses

Against this backdrop we’re likely to see large corporates pursuing value creation strategies to maintain cash flows. In cases where inflation could lead to negative real returns on investment in the short to medium term, this could result in further strategic portfolio reviews and the divestment of core assets. We also expect supply chain disruption to prompt targeted mergers and acquisitions as companies look for ways of making their supply chains more resilient.

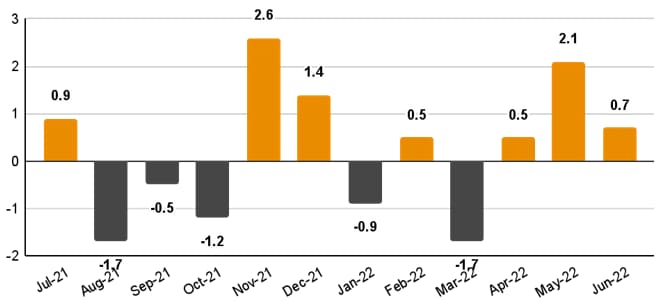

Euro Area Industrial Production, month on month % change

Source: Eurostat

Zooming in on Switzerland

With year-on-year increases in sales in the first six months of this year and high order levels suggesting that this trend will continue in the second half, Swiss manufacturing seems at first glance to be in good shape. But manufacturers in Switzerland too have also been hard hit by supply chain problems and rocketing energy and commodity prices. This is made even worse by the rapid nominal depreciation in the euro. All of these factors are leading to margin pressure. And there is the added risk that energy shortages will shut down production over the winter.

#social#

Contact us

Director, Co-Lead Performance & Restructuring, PwC Switzerland

Tel: +41 58 792 21 60

Claude Fuhrer

Partner, Global Health Industries Transformation Leader, PwC Switzerland

Tel: +41 58 792 14 23