The segments of pharmaceuticals and life sciences (PLS) as well as healthcare services (HCS) continue to face several headwinds. Macroeconomic factors such as slowing GDP growth, inflation and interest rate hikes, as well as geopolitical challenges have created a difficult environment for deals in 2022 – and we expect these challenges to diminish only slowly in the near future. Despite this backdrop, deal-making is likely to develop on a normal level in 2023 as PLS and HCS companies need to make acquisitions to realise their growth plans and gain access to innovative technologies.

While volatile markets and lower public company valuations in some cases limit the ability of companies to make large transactions, lower valuations of public companies also lead to opportunities for public-to-private or public-to-public transactions – especially in biotech, where Big Pharma strives to replenish and bolster the pipeline. PEs have abundant capital and will also actively pursue mergers and acquisitions in the healthcare sector this year. Although lower public company valuations may create opportunities to acquire innovative assets at attractive prices, valuations of truly innovative assets will remain high and buyers will compete for them.

Furthermore, supply chain disruption from the global pandemic and rising geopolitical tensions have led business leaders to re-evaluate the risks and dependencies within their global supply chain and turn to M&A to gain more control. We expect supply chains to become more on-shoring, near-shoring or "friend-shoring" through M&A to shorten lead times and provide more certainty to customers – and anticipate deals along the entire value chain, from raw materials to the distribution of products.

Global M&A trends in health industries Pharmaceuticals and life sciences (PLS)

Among large-cap pharma companies, we’re seeing interest in M&A opportunities to achieve their growth plans. They have a particular focus on midsize biotech companies (with a value of USD 5-15 billion) that can fill large players’ pipeline gaps in the coming years. But competition will be high since the biotech space only consists of a limited number of truly innovative companies available on the market. Combined with high valuations for such sought-after assets, this might entail more small and mid-range deals as well as collaborations (licensing deals, JVs, etc.).

As big pharma conglomerates continue to reshape and optimise their portfolios and to align them more closely with their core competencies, they are identifying non-core assets to divest. Their divestiture plans to generate cash for new investments may get tailwind from rising interest rates and declining share prices.

On the other hand, large corporates are competing with cash-rich PE funds, not only for biotech, but also for contract research, development and manufacturing organisations as well as medtech firms with strong cash flows. Competition for companies with mRNA or cell and gene therapy capabilities will be especially fierce.

Healthcare services (HCS)

Healthcare turning into a consumer good is an evolutionary trend. Companies offering vitamins, minerals and supplements (VMS) as well as nutraceuticals with high multiples will remain attractive assets in 2023, especially as recently divested pure-play OTC and consumer health companies seek to accelerate their own transformation plans through M&A. At the same time, PLS and HCS companies continue to modernise and digitise their business models with digital analytics technology, smart health devices, healthcare practice management software, and consumer-centric delivery models. Acquiring these capabilities is driving cross-sector deals, and PLS and HCS firms are looking to buy or partner with technology companies – also with startups – to leverage digital solutions.

The significant government support that certain healthcare sectors received during the pandemic has either ended or is being reduced. This could lead to an increase in distressed deals. Hospitals, for example, face major operational challenges because of persistent labour shortages, which could create liquidity challenges and force them to restructure or resort to M&A. Staffing challenges also put further pressure on healthcare providers to find patient-centric digital solutions for bridging the gap caused by a shortage of skilled employees. Telehealth, health tech, and analytics companies will continue to be attractive assets to invest in as a means to help fill these value gaps.

Health industries deal volumes and values, 2018-2022

"Macroeconomic conditions are likely to remain challenging in 2023. However, acquisitions will continue to be a popular option for healthcare industry players looking to realise their growth plans and innovate their business model. After the valuation levels have somewhat corrected last year, this will make a compelling case for M&A.”

And what about M&A in the Swiss health industry?

In 2022, while most of Europe and the world were hit by severe inflation and subsequent sharp interest rate hikes, the Swiss economy showed resilience thanks to its somewhat balanced industry landscape described by many as a refuge in times of economic turbulence.

In fact, in 2022, the Swiss pharma and life science industry has seen 103 M&A transactions with sellers or buyers based in Switzerland. After a record dealmaking in 2021 (139 deals), the widely expected dip in deal activity following the post-Covid 2021 frenzy and the start of the global disruption due to the crisis in Ukraine was less dramatic than many expected. However, while deal volumes declined only slightly, deal values saw a more significant drop.

Nevertheless compared to 2018 to 2020 – when deal activity doubled to 100 deals per year –, the past year has added to the long-term upward trend in M&A activity in Swiss health industries.

Swiss health industries deal volumes and values, 2018-2022

In my last blog post in August 2022, I concluded that – despite significant macroeconomic headwind from higher interest rates and inflation – M&A transactions remain a crucial source of corporate growth and will therefore continue to be relied upon as long as the economic outset is structurally intact. In 2022, we saw that health industries and especially health services remained attractive due to their resilient nature, while the more risk-prone biotech deals recorded a slight decline.

What’s trending in Swiss Health Industry M&A?

Biotech, medical device and pharma deals have accounted for roughly two thirds of health industry deals. The remainder reflects takeovers and divestments in the area of laboratories, nursing facilities, as well as hospitals and practices (health services).

Compared to 2021, the number of pharma & life science deals decreased by 30%, while health service deals dropped by 15%. In the absence of mega-deals (deal value in excess of USD 5 billion), the data reveals that 2022 has been a year of smaller deals. This can be explained by large corporates exhibiting caution when considering resource allocation and by the fact that available targets are primarily early stage assets. Furthermore, private equity houses were re-thinking their acquisition strategies in light of debt-market uncertainties and spending their funds rather on smaller businesses. As a result, the times of mega-deals in large numbers seem to be a story of the past.

Biotech ETFs as a proxy for company valuation

However, after the spike in 2021, biotech valuations have come down and stabilised in 2022. As predicted, this helped corporates to return to dealmaking; and with their strong balance sheets, we see corporates well positioned to accelerate M&A again in the coming year(s).

Swiss PLS deal volumes and values, 2018-2022

In biotech, we see that large corporates have continued to invest in future capabilities and made strategic additions to their existing portfolio. The urge to fill the pipeline, take shortcuts in drug development and secure future profits drives the thirst for external growth especially in times of high competition from biosimilars for traditional pharma. Recent examples of capability-driven investing include Alcon’s acquisition of Aerie Pharmaceuticals in the UK and Roche’s takeover of Good Therapeutics. Besides, venture investments undertaken by corporate VC funds have added to Swiss deal flow.

In the pharma space, the larger deals were transactions with private equity involvement and often reflect smaller service providers or clinical stage biotechs within the Swiss pharma cluster. This trend of (smaller) financial investments in growth cases is expected to continue as venture capital and private equity investors still have large funds to deploy despite higher interest rates.

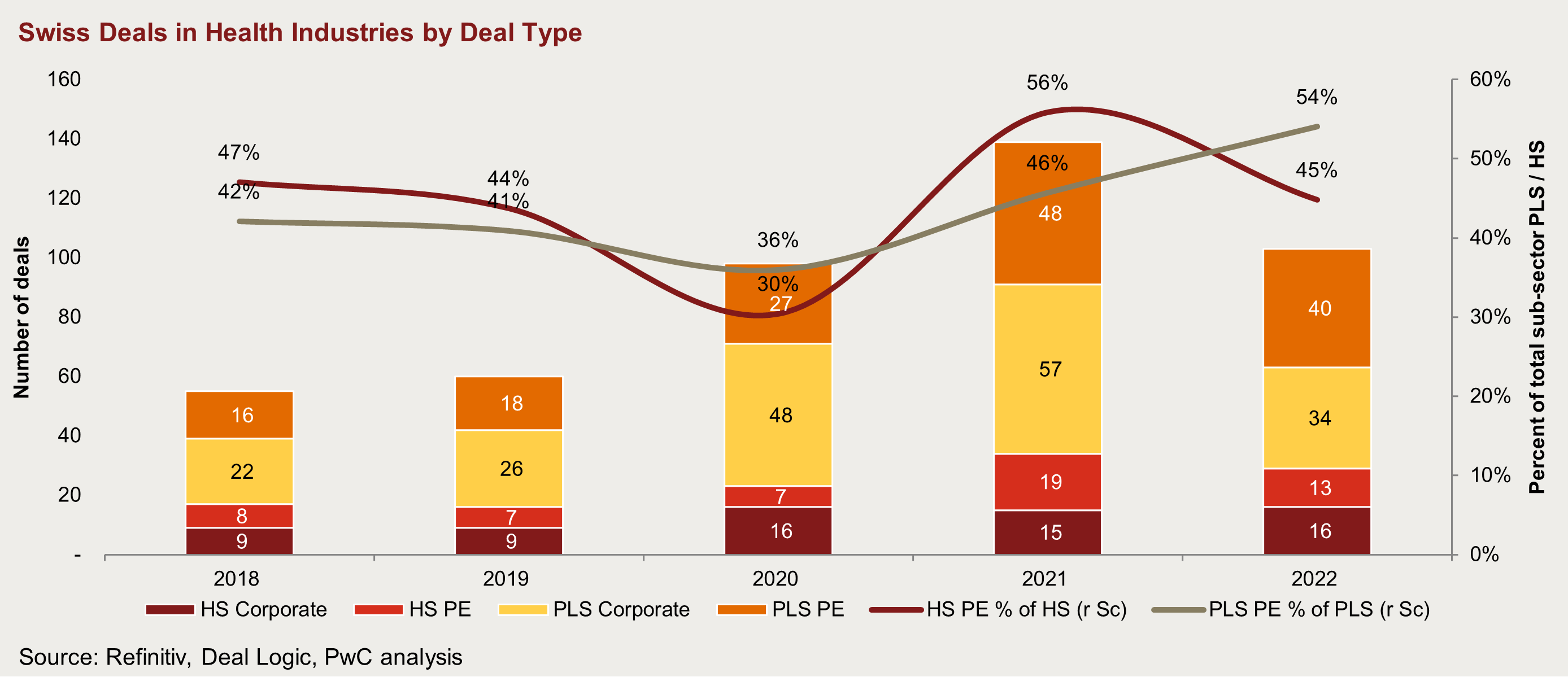

Swiss deals in health industries by deal type, 2018-2022

Despite lower deal volumes than in 2021, the role of financial investing in Swiss health industries has been persistently high in 2022; about 50% of all Swiss deals involved private equity investors. In light of the central banks ending the ultra-expansive monetary policies worldwide, which put an end to the seemingly endless funding taps, one can argue that the persistently high number of private equity deals reflects the resilience of the sector and is a reason for optimism. Although the deals might be smaller and more selective, investing in health industries remains a crucial pillar in private equity portfolios.

Top M&A Deals of Switzerland in 2022

| Buyer | Target | Deal value | Timing | Comment |

| Cordis Corp | MA Med Alliance SA | 1'135 | Q4 | Swiss-based medical technology company MedAlliance has announced it has entered into an agreement with Cordis for an acquisition |

| Groupe Bruxelles Lambert SA | Sanoptis AG | 809 | Q2 | Groupe Bruxelles Lambert has signed definitive agreements to acquire a majority stake in Sanoptis, a leading network of ophthalmology clinics across Germany and Switzerland, from Telemos Capital. |

| Alcon AG | Aerie Pharmaceuticals Inc | 753 | Q3 | Alcon and Aerie Pharmaceuticals, a pharmaceutical company focused on the discovery, development, manufacturing and commercialization of ophthalmic therapies, today announced the companies have entered into a definitive merger agreement through which Alcon will acquire Aerie. |

| Sonova Holding AG | Alpaca Audiology LLC | 310 | Q1 | Sonova Holding, a leading provider of hearing care solutions, has signed an agreement to acquire Alpaca Audiology, one of the largest independent networks of audiological care clinics in the US. |

| Roche Venture Fund | Freenome Holdings Inc | 290 | Q1 | Freenome, a privately held biotech company with a comprehensive multiomics platform for early cancer detection, announced today that Roche has made an investment of $290 million. |

| Roche Holding AG | Good Therapeutics Inc | 250 | Q3 | Roche has signed a definitive merger agreement for the acquisition of US-based biopharmaceutical company Good Therapeutics for an upfront payment of $250m in cash. |

2023 outlook: health industry M&A is set to rebound, with investors attracted by innovation and growth prospects

We expect dealmaking activity in health industries will stabilise in 2023 as investors remain attracted to the sector despite the uncertain macroeconomic conditions. Companies that use M&A as a tool to transform or reposition their businesses will be well placed to create long-term value and sustained outcomes for their stakeholders.

What’s the 2023 outlook for mergers and acquisitions in Switzerland’s health industries?

After the world economy has come under the threat of inflation, shortages and higher interests in 2022, economic indicators for 2023 remain challenging. But with receding uncertainty and the structural economic framework being intact in Switzerland, there is some optimism that the dark clouds will be less in 2023. Big Pharma is hungry for strategic pipeline additions to secure future profits, and PE houses have dry powder with health industry assets high on their priority list. Based on these tailwinds and coupled with an expected easing of debt markets, we are positive about 2023 and expect M&A in the healthcare industry to remain on top of investors’ wish lists.

PwC ranked #1 Global and Swiss M&A Advisor by Volume for 2022

Our PwC Corporate Finance team has ranked as the Global and Swiss #1 M&A Advisor by Volume for 2022 by Thomson Reuters, Bloomberg and Dealogic.