On November 20th the European Commission proposed amendments to the Sustainable Finance Disclosure Regulation (SFDR) which would introduce a new prescriptive framework for sustainable finance. The reforms move the SFDR from a disclosure regime to a product categorization system, with prescribed thresholds, exclusions, and transparency duties. For financial market participants (FMPs), the implications are significant: product strategy and governance, reporting processes, investment due diligence and data management will all require substantial redesign.

While the proposal reduces entity level reporting obligations and narrows down the scope to exclude portfolio management mandates, financial institutions will still need to consider the revised framework and determine how these shifts reshape their sustainability strategy and their product portfolios.

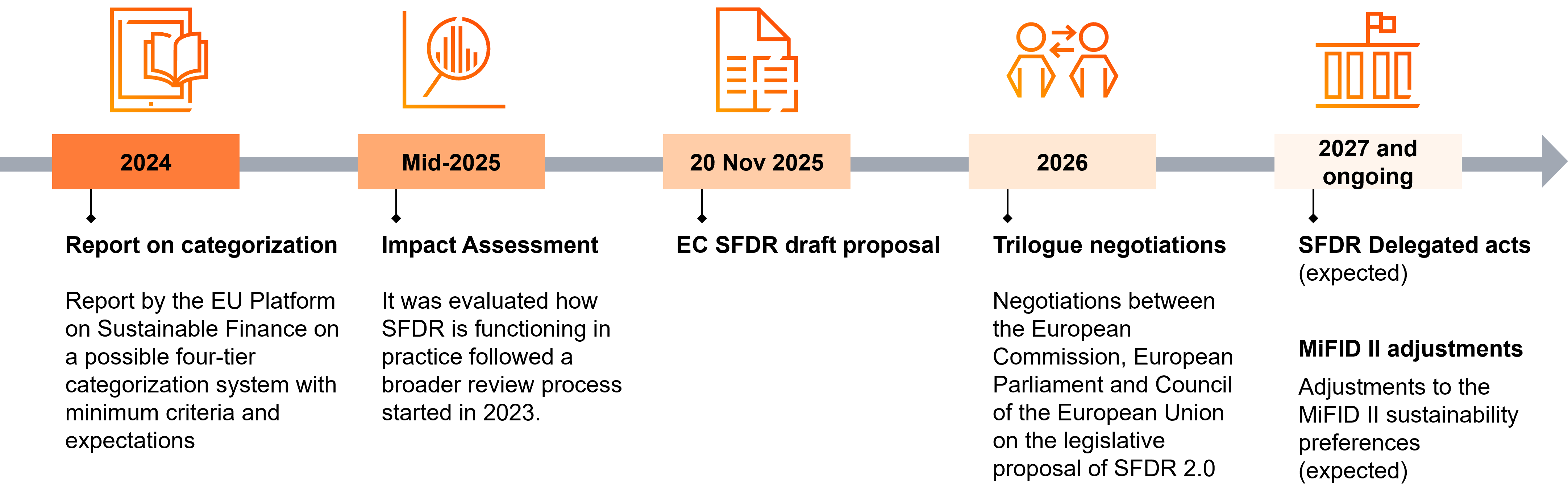

Expected regulatory timeline

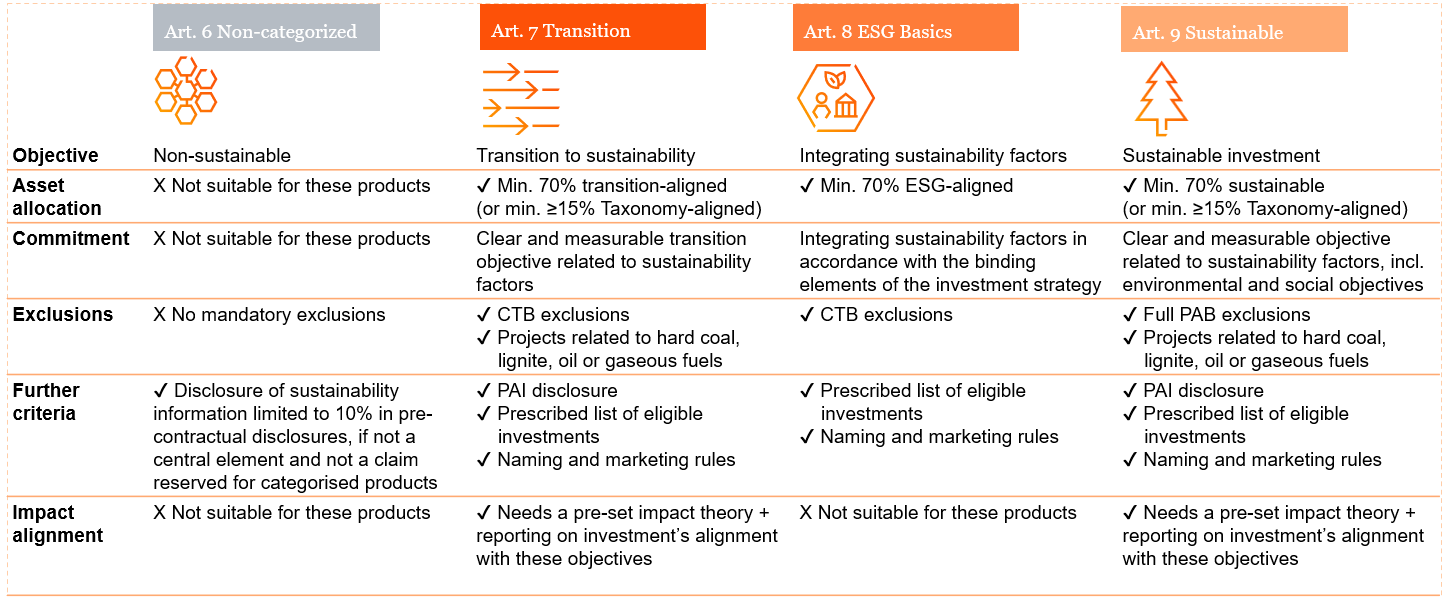

Shift from a disclosure to a categorization regime with three new product categories

The introduction of a dedicated transition category marks a notable shift in the revised SFDR framework. For the first time, products investing in activities that are not yet green but are moving in that direction have a clearly defined place. This fills a long-standing gap in the market where transition-focused strategies often struggled to fit within the previous Article 8 and Article 9 structure.

Transition Category (Article 7)

Products that support environmental or social transition, with most investments tied to a clear transition objective and subject to strict exclusion rules and principle adverse impact disclosures.

ESG Basics Category (Article 8)

Products that integrate sustainability factors in their investment process, meeting a minimum investment threshold and standardised exclusion criteria.

Sustainable Category (Article 9)

Products that primarily invest in activities with measurable environmental or social objectives, following the most robust exclusion rules and reporting on their principal adverse impacts.

Overview of key product category criteria

Introduction of a New “Impact” Sub-Label

The proposal adds a new “impact” designation for transition and sustainable products that target a clear, measurable environmental or social outcome. Products using this label must define a pre-set impact theory and report on how their investments deliver against those objectives.

Ahead of the Curve: PwC’s Approach to Navigating SFDR 2.0

The draft regulation must now move through the EU legislative process, which may lead to further changes. Once finalised, it will apply 18 months after its publication in the Official Journal. As a result, implementation of SFDR 2.0 remains some distance away; however, the breadth of the proposed changes makes early preparation essential.

The new framework does not include a grandfathering regime, meaning that existing funds will also need to comply once the rules take effect. The only exception applies to closed-ended funds that are no longer being distributed after the revised SFDR comes into force.

To start assessing readiness, firms can already consider the following questions:

- How will our existing products map to the new Article 7, 8 and 9 categories, and what strategic or design changes might be required to meet the associated thresholds and exclusions?

- Are our sustainability claims, marketing materials and naming conventions fully aligned with the revised restrictions?

- What updates to website disclosures and internal governance will be needed to support the new, streamlined pre-contractual and periodic reporting requirements?

This analysis will help firms identify the operational, data, and governance changes required to transition smoothly into the revised SFDR framework, in preparation for further clarifications brought by the future Delegated Acts.

By partnering with PwC, financial institutions can confidently move beyond legacy SFDR approaches and adopt a future-proof compliance framework—empowering them to take proactive steps in sustainable finance while staying well-positioned to navigate evolving regulatory requirements.

Get in touch with PwC today to begin your seamless transition to the new SFDR framework and turn regulatory change into a strategic advantage.

Contact us

Jack Armstrong

Patrick Schmucki

Sofia Jaccard

Tina Minci