The TMT sector is undergoing rapid change, driven by new technologies and consumer demands. This will continue to provide plenty of M&A opportunities. Against the backdrop of a challenging economic environment, we expect dealmakers to be more cautious in 2023. The bar for deals will be higher, particularly for larger deals that may attract greater regulatory attention. In Europe, regulators’ anti-monopolistic agenda has blocked mergers of equals in the media industry where consolidation is viewed as crucial to competing with international players. Data privacy remains a core issue.

Dealmakers may want to target companies that either starve for capital or offer a value-enhancing platform or technology. We expect an increase in public-to-private transactions in the coming months, as well as opportunities for cash-rich companies and investors to take advantage of lower asset prices. While more expensive capital will impact transaction values, particularly for high-growth companies focused on revenue growth and customer acquisition, this bodes well for opportunistic M&A in the near term, and we are likely to see an increase in joint ventures (JVs), partnerships, and other arrangements to get deals done.

Infrastructure-enabling technologies remain a hot topic, with consumer demand leading to attractive M&A opportunities along the value chain. We're seeing the continued adoption of digitally-enabled experiences across all segments of the TMT sector – from software and semiconductor technology to next-generation fibre networks, IoT and data centre capacity to the future of gaming. For investors wanting to deep-dive into the space of augmented and virtual reality, the metaverse provides an innovative way to position companies’ brands and solutions for future success. It attracts corporates seeking a first-mover advantage, which will drive M&A activity.

What drives M&A in tech, media, and telcos in 2023?

Technology sector

Software will continue to dominate TMT M&A. PE investors accounted for 50% of software deals in 2022 and this is expected to continue, driven by the attractive business models of software companies that combine predictable and growing revenues, high margins, and strong revenue generation.

In IT services deals, cyber security, DevOps, software development, digital transformation, and low code will be key topics for 2023. In these segments, growth and margins are above trend as organisations undergo digital transformation and security risks continue to grow.

Semiconductor deals are likely to be subdued in 2023. Several blockbuster deals were not closed due to antitrust and national security concerns, for example US-based Nvidia’s attempted acquisition of UK-based ARM and China’s Sai MicroElectronics’ attempted acquisition of Germany-based Elmos Semiconductor. Chip shortages and supply chain issues will likely force non-semiconductor businesses reliant on chips to consider acquisitions for greater control of design, intellectual property, and supply.

Following Elon Musk’s USD 44 billion acquisition of Twitter, internet dealmaking is also expected to be slower in 2023. Advertising revenue streams and subscriber growth might be affected by consumers’ budget constraints due to inflation. Furthermore, regulators’ increased focus on data privacy, child safety, and competition is adding costs and constraints to internet business models.

Media enterprises

Customer demand for live sports has been a consistent deal driver from team sales to advertising. In the National Football League, the Denver Broncos franchise sold for a record amount, and initial estimates for possible upcoming sales of other high-profile sports teams highlight the unique value these “trophy” assets can generate. In tandem, ongoing interest in sports gambling, data analytics, and live content rights will continue to make this an acquisitive sector.

An ever-changing ad market that was disrupted by the pandemic and the rollout of advertising-based video on demand (AVOD) will continue to drive innovation in ad-tech, engagement, and measurement. Maintaining a competitive position and access to individual walled gardens could drive M&A, as companies look to scale their reach and customer pool through deals.

Telecommunications

Consolidation continues to be a theme in telecom. In the mobile segment, competition created by multi-player markets incentivises capital deployment in network capabilities. In the fixed-to-mobile segment, operators seek to benefit from network, customer, and proposition synergies. Fragmented fibre markets and mobile towers will see consolidation – also driven by distress and constraints on access to capital – as operators seek to reach scale and achieve rollout targets.

Given higher financing costs and significant capital expenditure demands, telcos will continue to divest non-core and asset-heavy divisions, allowing them to generate cash and deleverage. Broadly, telcos will look to monetise non-core IoT, media/content, advertising, and B2B information and communications technology (ICT) divisions through spinouts.

Telecom operators will seek tech convergence to pivot towards higher growth revenue streams through capability-driven M&A, with data analytics, cyber security, and cloud segments all considered strong candidates for activity. Thereby, user interface and back-office infrastructure – while not typically making the headlines – are necessary to ensure that underlying tech powering consumer and B2B solutions are best in class and will take place in 2023.

Technology, media and telecommunications deal volumes and values, 2018-2022

Sources: Refinitiv, Dealogic and PwC analysis

TMT deals were responsible for more than a quarter of all transactions in 2022 – in terms of volume and value – and dominated the global transaction market. However, the M&A environment cooled somewhat in the second half of the year against a backdrop of rising interest rates, geopolitical tensions, and concerns about a recession. Overall, 2022 TMT M&A deal volume declined by 21%, and deal value fell by 36%, but both levels remain well above pre-pandemic levels. Opportunities still exist for mid-sized and smaller transactions made by corporates with enough cash.

"Digital disruption and the search for improved user experience continue to drive the TMT market. M&A activity in 2023 will be driven by opportunistic players looking to solidify their strategic position."

M&A developments in the Swiss TMT sector

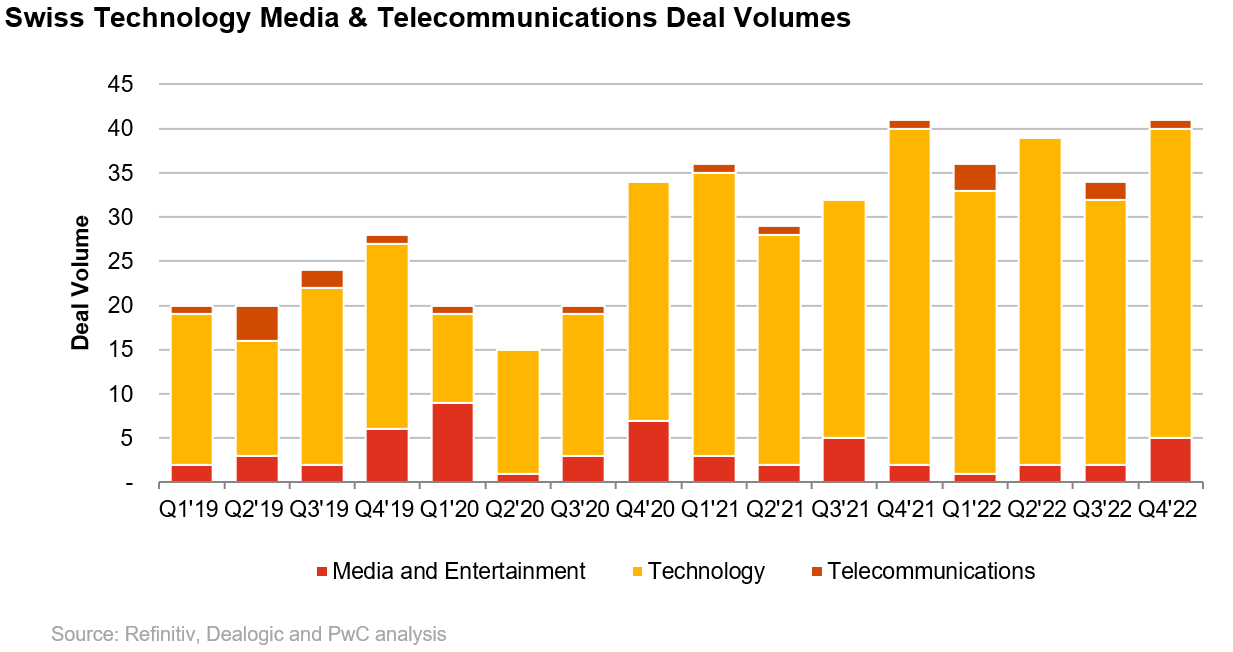

While global markets (–21% YoY) and to a lesser degree European markets (–8% YoY) saw a significant drop in TMT-related M&A activity in 2022 – following a historically strong 2021 –, the Swiss market was exceptionally resilient, with M&A activity involving Swiss TMT companies reaching an all-time high (+9% YoY). Benefitting from lower inflationary pressure and an overall better macroeconomic environment than in many neighbouring countries, the Swiss market saw a record number of 150 transactions involving TMT target companies last year.

As in prior years, transactions involving software companies built the backbone for Swiss TMT M&A deal activity, accounting for more than two thirds of all TMT deals, while IT services companies were the second largest driver and responsible for 13% of transactions. Overall, technology in TMT remains king in Swiss deals, with almost 90% of all TMT M&A activities being related to technology assets. While many global tech stocks have seen a significant drop in valuations, software companies remain attractive M&A candidates, particularly in the cloud, analytics, collaboration, and security sectors, supported by stable growth factors, attractive business models, and room for consolidation. As a result, we expect the software sector to continue to drive TMT M&A activity in Switzerland in 2023.

With strong underlying fundamentals, it comes as no surprise that the TMT M&A space in Switzerland saw again significant interest from private equity (PE) and financial investors with almost 50% of transactions involving a financial sponsor in 2022. This number is up from only 20% in 2018 and similar to what we observe on a global level in the TMT sector. The comparison with all other sectors in Switzerland, where PE accounted for an average of only one third of transactions last year, underlines the special attractiveness of the TMT industry for financial investors. And while fundraising by European private equity funds has slowed significantly in 2022 (to levels last seen in 2014), we expect the remaining "dry powder" to continue to drive transaction activity from this group of buyers.

But it is not only in terms of the role of financial investors that the TMT sector defies Swiss standards: while in non-TMT sectors foreign and Swiss buyers accounted for an almost equal share of transactions in 2022 on average, in the TMT sector 61% of all assets went to foreign buyers (a slight decline from the all-time high of 65% in 2021). This underlines the attractiveness of Swiss TMT assets for foreign buyers and the sector’s stronger international perspective compared to more inward-looking industries.

Likewise, and comparatively different, non-TMT buyers continue to play an important role for transactions in the TMT sector, with 63% of all transactions completed in Switzerland involving TMT targets going to non-TMT buyers in 2022. In comparison, in all other sectors the majority of last year’s transactions were completed by a buyer from the same sector in Switzerland. This trend of sector-foreign buyers in the TMT market has remained stable in recent years. Given the constant need for companies to innovate and digitise, we therefore expect non-TMT buyers to continue to turn to TMT assets.

In Switzerland, we expect TMT targets to remain in the focus of dealmakers despite uncertainties.

Despite a turbulent 2022, which amongst other factors saw rising interest rates, the invasion of Ukraine (having a big cohort of skilled software developers), and fears of an energy crisis in Europe, TMT dealmaking showed extraordinary resilience and reached an all-time high in Switzerland last year. While mega-deals may be hampered by the ongoing uncertainty in global markets in the next months, we believe that the continued strength of fundamentals and interest from financial investors and foreign buyers will continue to drive dealmaking in the Swiss TMT market in 2023. Given the decline in tech valuations in global markets, we also expect buyer and seller expectations to converge in the coming months and especially high-value assets to remain in high demand.

Although a major unexpected shock to the system can never be excluded, the TMT market in Switzerland has shown that M&A activity remains high even in times of uncertainty and economic turmoil. For this reason, we expect transaction activity in the technology, media, and telecom sector in Switzerland to continue at a similarly high pace, at least in the coming months.

2023 outlook: M&A in tech, media, and telcos will be driven by both strategic and opportunistic deals while capital discipline remains key.

Experienced dealmakers can take advantage of the sector's evolution and dynamics and strengthen their market position with new technologies, platforms, and solutions. Corporates with strong balance sheets and access to capital have the opportunity to enhance their portfolios and pursue their strategic goals, driving long-term growth and capabilities across sectors. Joint ventures (JVs), partnerships, and other arrangements may increasingly be used to execute deals.

PwC ranked #1 Global and Swiss M&A Advisor by Volume for 2022

Our PwC Corporate Finance team has ranked as the Global and Swiss #1 M&A Advisor by Volume for 2022 by Thomson Reuters, Bloomberg and Dealogic.