Private banks as well as private banking divisions of universal banks across the globe have seen a continuous rise in assets under management (AuM) driven by strong market performance, rising wealth of high-net-worth individuals (HNWIs) and acquisitions (see our article Global private banking – seeking growth beyond markets). Despite this comfortable positioning, only limited progress has been achieved on feeding growth through to the bottom line. This is because two thirds of growth in operating income has been absorbed by cost increases (see Exhibit 1 below). However, a few private banks have outperformed their peers, managing their bottom line in a balanced way and achieving superior results.

Exhibit 1: Global average business metrics

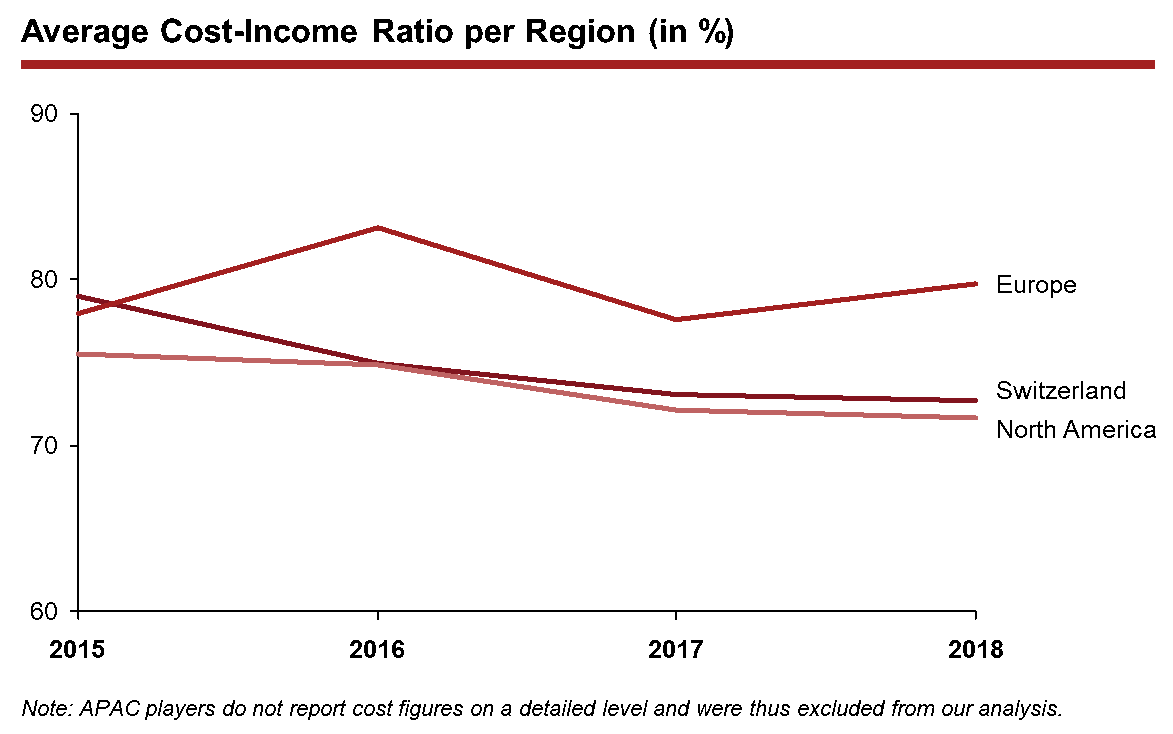

The quest for improved cost-income ratios in private banking

Within our data set of more than 30 private banks, there are considerable differences across regions, with European (in particular German) private banks reporting the highest cost-income ratios (CIRs) coupled with limited progress in decreasing costs. Swiss and North American private banks achieved fairly similar cost levels, driven by continuous efforts to reduce costs in recent years.

Differences in cost levels between regions and individual players can be traced back to regional regulatory restrictions (e.g. prohibiting specific income streams or higher administrative costs for regulatory reporting) and differences in specific business models and market approaches (e.g. high-touch vs. low-touch).

At individual bank level, Intesa Sanpaolo leads the group with their private banking division achieving a CIR of 32% in 2018. Intesa Sanpaolo’s private banking division benefits from the overall low cost structure of the universal bank and continued efforts to decrease its cost base. Credit Suisse and Julius Bär, two Swiss players, achieved the biggest decrease in their CIRs – both by a compound annual growth rate (CAGR) of 7% over the last three years. These decreases were mainly achieved through considerable cost management programmes at both banks, which led to lower or stable absolute operating costs.

Exhibit 2: Average cost-income ratio per region

Our analysis has found that although slimmer in size and specialised in their business model, pure play private banks do not benefit from a cost advantage on an aggregate level (see Exhibit 3). In fact, private banks in our data set do not seem to capitalise on leaner and more efficient operations, or this effect is offset by the scale efficiencies enjoyed by private banking divisions of universal banks. Furthermore, pure play private banks have higher personnel costs, on average, than private banking divisions of universal banks. This can be attributed both to pure play private banks’ tendency to allocate higher wages to their front-office staff and to universal banks needing fewer staff as they can spread tasks across divisions (e.g. co-coverage of investment functions between private and investment bank).

Exhibit 3: Cost-income ratios of private banking divisions and pure play private banks

Profitability leaders actively address their cost base and achieve considerable cost advantages

The majority of private banks in our data set have addressed their cost base and across the data set, CIRs went down by an average of 6.3%. However, the profitability leaders outperformed this average by decreasing their CIRs by almost 7% over the past three years. The “bottom 5 performers”, on the other hand, actually registered an increase in their cost base of 6.7% on average. At individual bank level, profitability leaders were able to decrease CIRs with a CAGR of between 2% and 8% from 2015 to 2018. This leaves them with considerable cost advantages over their peers, resulting in higher net margins and operating profits.

Exhibit 4: Cost-income ratios of profitability cohorts

In absolute terms, private banks’ operating costs increased by a CAGR of 4% between 2015 and 2018, whereas profitability leaders saw only a marginal increase by a CAGR of 2% in the same period – despite substantial AuM and income growth. On the other side, the “bottom 5 performers” registered an average increase in operating costs by a CAGR of 5% combined with sluggish AuM growth (some even with slight decreases) and continuous margin compression, resulting in an increase in CIRs.

Striving for balanced cost reduction

For years, private banks – in line with the overall industry – have increasingly focused on lowering costs. However, although cost reduction has a direct impact on private banks’ net margins, spending too little might hamper top-line growth. Our data (see Exhibit 5) suggest that banks with reasonable, but not the highest, cost decreases achieve higher revenue margins and thus capture more business than those that have decreased their CIRs the most.

Exhibit 5: Relationship between change in CIR and revenue margins per private bank

Reducing costs in a balanced and targeted way seems to be the best approach as high revenue margins seem to favour a balanced CIR (see Exhibit 6). In fact, profitability leaders increased their spending on personnel, while decreasing their general and administrative costs over the three year period, indicating that they took a balanced approach to cost reduction.

Exhibit 6: Relationship between private banks’ CIR and net margin

Managing the bottom line requires a holistic and tailored approach

As demonstrated by our analysis, a holistic yet tailored approach to cost management will drive profitability for private banks, while broad-based cost-cutting could potentially hamper top-line growth. Thus, for a private bank to be successful, it is essential that it preserves “good” costs that enable future business growth and cuts “bad” costs using strategic cost-cutting measures. To do this, banks can use several measures from within the cost management toolset, including: i) portfolio and capability selection (“What?”), ii) organisation and location (“Where?”) and iii) operational excellence (“How?”). Exhibit 7 provides an overview of our Fit For Growth toolset for cost management, parts of which are further elaborated on below.

Exhibit 7: Overview of the Fit For Growth toolset

The “What?”:

- Portfolio rationalisation: Portfolio rationalisation is where you identify the business lines, products, customers, channels and geographies in which complexity is driving high costs and then remove both the costs and the underlying drivers of complexity. The goal is to reduce complexity that is not adding value. The process should focus on products and/or client segments that are central to the bank’s/ division’s strategy. Credit Suisse, for example, exited their US business, while Julius Bär increased their focus on core client segments and geographies (e.g. (U)HNWIs and divestment of asset management business in 2009).

The “Where?”:

- Operating model: The operating model defines where critical work gets done, how organisational units are structured and how people work together. The goal is to align a private bank’s operating model with its strategy to directly support areas of differentiation that are vital for its profitability. For instance, ecosystem approaches, whereby certain products are sourced from other players, are increasingly gaining traction. This approach is exemplified by digital challengers who focus on the customer interface and aggregate third party products (e.g. TrueWealth). Furthermore, in recent years some private banks have successfully narrowed their focus, such as Vontobel, which placed a clear focus on advisory and wealth management while concentrating its booking centres or leveraging partner banks within its operating model for local booking (e.g. in New York).

- Outsourcing/offshoring: Like other financial service players, private banks can decide to run necessary but non-differentiating tasks by themselves or hand them over to external service providers. Both options can be done on-shore (benefiting from factor cost advantages) or off-shore. Furthermore, recently emerging utility concepts aim to centralise non-differentiating support functions across multiple players within the financial service industry and specific regions, providing added value (e.g. higher quality) as well as cost benefits.

The “How?”:

- Process excellence: A process excellence initiative can identify the true sources of customer value in a product or service and determine which processes create that value and how. Other processes can then be simplified or eliminated. A private bank should strive to radically optimise its processes to reduce the cost of delivery of its services (e.g. regulatory and compliance processes).

- Digitalisation: Digitalisation involves the use of a wide variety of technologies to automate manual tasks, analyse large amounts of customer and market data, and manage complex business processes. Its proper use can reduce costs and improve the quality of both internal processes and interfaces with customers, service providers, and other outside parties. Large-scale process automation and artificial intelligence (AI) can have a high impact on private banks’ cost base – and is especially important for pure play private banks that cannot leverage established middle and back-office functions that universal banks have. Thus, several players have intensified their efforts in this area. For example, Wells Fargo launched a dedicated digitalisation initiative in 2017 to increase speed and convenience for its internal teams. In addition, ABN Amro invested heavily in digitalising its organisation and internal processes (spending €170m overall in 2017) and now offers an increasingly broad array of digital services within its private banking division.

Key takeaways

Although the private banking sector has recorded a decade of growth and some progress has been achieved in managing the bottom line, there is an opportunity to achieve above-average margins and improve current profitability levels by applying a holistic and forward-looking approach to cost management.

Furthermore, bumpy roads lie ahead for private banks due to challenging markets, the risk of intensifying trade wars and the entrance of streamlined challenger banks, all of which will reinforce the pressure on margins. In this environment, reviewing and transforming a private bank’s cost base can complement top-line measures to preserve margins and equip them fit for future growth. Selecting the right initiatives from the cost management toolset and making data-driven decisions will give a bank a competitive edge and build a solid base from which to compete in the years ahead.