{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

The television advertising market encompasses all advertising spending via broadcast or online television within, before and after TV programmes. TV advertising comprises revenues generated by free-to-air networks (terrestrial), cable, satellite and Internet Protocol TV (IPTV).

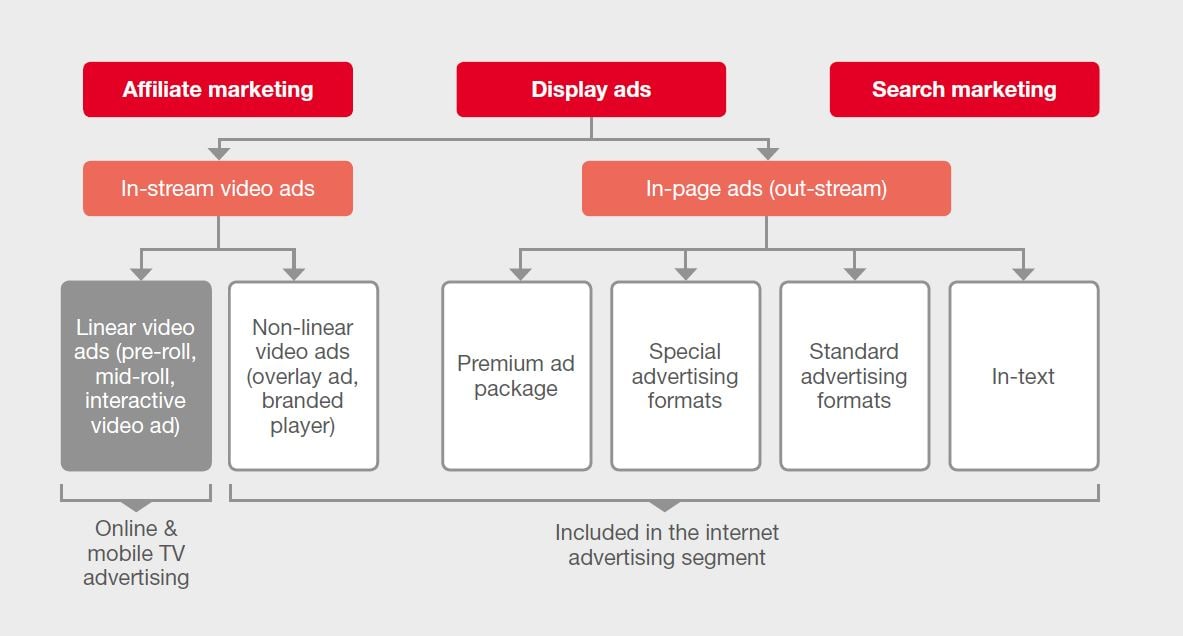

Online and mobile TV advertising consists of linear in-stream adverts only (combining pre-roll, mid-roll and post-roll revenues). Not included are the following components: non-linear adverts (such as overlay ads, where advertisers use a video overlay to deliver an ad unit) and in-page ads.

Within linear in-stream adverts, only revenues from broadcast TV viewed on TV websites and internet TV platforms such as Teleboy or Wilmaa are taken into account; the type of device is irrelevant.

Video content consumed via other platforms such as YouTube are not covered, as these revenue streams are part of Internet Advertising. All TV advertising figures are shown as net revenues, excluding agency commissions and discounts.

Traditional TV advertising is being forced to adapt to modern industry standards where digital video recording and time-shifted viewing are becoming the norm. The range of video streaming services is growing and more and more people are watching TV in replay mode which allows them to skip the commercials. As a result, TV stations lose millions of advertising revenue. Spott, a Belgium-based start-up, is testing a creative way to get the viewer’s attention by shifting the emphasis of advertising, namely to pull rather than push. Spott is approaching a new TV advertising future that capitalises on multi-screen usage and monetisation through high user engagement. The application allows users to interact directly with TV shows via a second screen and purchase items they see on the show. This allows consumers to interact with the brand content that appeals to them, rather than being spammed with ads they have no interest in. The challenge is to find a happy medium where content attracts attention, yet the product does not distract from that content.

By synchronising handheld devices with programmes, it becomes possible for viewers to engage in an item of interest, for example the new jeans of your favourite TV show’s main character or his best friend’s stylish watch, and not just with ads provided by companies. The business model is B2B as well as B2C. It gives viewers access to offers while they watch TV shows, and the providers receive their cut. To make this possible, it takes deals with brands, broadcasters and content creators. The result for brands and broadcasters is an increased viewership with higher engagement, which in turn yields a higher ROI compared to traditional advertising.

This technology is creating synergies with current business models. Providers of targeted advertising or content creators/providers are supported by smart technology like Artificial Intelligence. They display audience-tailored content, which improves the user’s experience, and this with the intent to activate the viewer’s engagement. Additionally, firm data regarding clicks, purchases and popular items allow companies to develop better content strategies. This technology could bring a fresh breeze into a challenged Swiss TV advertisement market, where there is an increasing trend to time-shifted TV consumption.

The broadcasting sector’s main source of income is the offering of advertising slots that focus on certain programmes, airing time or a specific target group. This market includes Swiss public and private channels as well as foreign TV companies with dedicated Swiss advertising windows.

In the online and mobile television sector, there are certain online or over-the-top (OTT) providers such as Teleboy or Wilmaa, as well as traditional broadcast channels that feed video content to laptops or mobile devices by means of open Internet networks. Advertisement slots are sold to finance their business.

Broadcast advertising and sponsoring revenues

Switzerland’s broadcast TV advertising revenues were reported by 62 channels in 2017, several more than in the two previous years. In total, these broadcasters earned net revenues of CHF 774 million, a decrease of CHF 17 million over 2017. This equates to a 2.1% decline compared to the 4.6% rise in 2016. Broadcast advertising generated CHF 725 million, while the broadcasting sponsorship revenues decreased from 56 to CHF 49 million in 2017. The latter represents a decline of -12.5% following the 7.7% growth recorded in the sports year 2016. This trend reversal was also due to 2017 not being a “Sports year”, which has always had a big impact on advertising budgets, spot sales and sponsorship (product placement).

The breakdown of net broadcast advertising revenues by channel type reveals the following: Swiss private channels recorded impressive growth of +15.3%. Private foreign advertising windows were also in the black (+3.9%), while sales by Swiss public broadcasters declined by 8.4%.

Foreign private channels were able to increase their advertising revenues and, with a 43.3% share of the market, overtook the public TV channels, which suffered a decline of 8.4%. Public TV channels garnered a 42.6% revenue share. Private Swiss broadcasters recorded a significant increase in their advertising sales (+8.9%) and accounted for 14.1% of total TV and sponsoring revenue. Within the online and mobile television advertising market, the positive revenue trend continued. According to the latest estimates for 2017, total Swiss advertising revenues in the online video market amounted to CHF 13.1 million.

Long-established revenue streams in the industry are being challenged as 2017 was the first year in which digital ad spending surpassed traditional TV advertising spending. Online advertising is expected to outspend TV advertisers by $40 billion worldwide in 2018. The Association of Swiss Advertisers market survey of 2017 noted that the three biggest challenges for the industry were the complexity of digitalisation, the fragmentation of the media channels, and a change in media usage.

Fusion of Classic TV Ad and Online Video Ad

TV advertising remains important because major advertisers are still planning big budgets earmarked for traditional channels like TV. They are familiar with TV as an advertising format and can rely on transparent, long-established metrics. TV makes it possible to reach a wide audience quickly and cost-effectively. Nothing sells better than sight, sound and motion. That's why many direct-to-customer brands are building their business with TV ads. TV advertising is a fast way to promote a product or service to a broader viewership. Above all, so-called “low-involvement products” require TV as an advertising format that offers the emotionality of video.

“TV ads and special ads achieve the strongest branding impact in the marketing mix. To build a powerful brand image in the Swiss market, it is unavoidable to use TV as an advertising channel to reach a wide audience.”

In Switzerland, classic linear TV advertising is no longer regarded as a stand-alone advertising channel. TV advertising has continuously moved to its own digital version. Time-shifted viewing, streaming and mobile consumption allow viewers to enjoy the desired content more flexibly. Younger generations, the digital natives, are keen on consuming content anytime and anywhere. TV will become even more fragmented by the increase of various new private channels, and time-shifting is gaining importance also for TV consumption on today’s super-sized screens.

TV is switching from digital cable to IPTV. Improvements are being made continuously and additional companies could opt to revert to more trustworthy advertising channels like TV in its new digital version.

"TV is an efficient medium with a wide reach and will therefore remain an attractive advertising channel. However, the TV screen in the living room is increasingly performing the function of a large tablet, e.g. by displaying broadcasts and long-form video via IP. In order to exploit the full potential of TV advertising, marketing must increasingly take online options and the multitude of devices into account.”

Currently the trend is going towards “moving-image advertising” concepts. Advertisers barely distinguish between TV and online video campaigns. For them it is important to achieve high coverage flexibly via TV and video, a strategy aimed at reaching a comprehensive target group. To fulfil this demand, it must be made possible to sell the combination of video and TV. While online advertising can compensate for the disadvantages of linear TV, advertising should be target-group-specific, but only to the extent that the user does not feel disturbed.

"Television and online video have grown together and should not be regarded as separate ad formats anymore. Advertisers want to gain significant impact and wide reach. This can be achieved by combining TV and online video advertising on various devices.”

Successful interactive TV in a “lean-back”-mode

Television is considered a lean-back medium, one that involves a minimum of interaction with the viewer, who passively watches the screen and is waiting to be entertained. Choosing a broadcast format in a media library is not seen as overly engaging, but is rather taken for granted. The viewer does not have to overcome any hurdles, as the use of video-on-demand platforms and media libraries has long since been a basic offering of all providers. Various applications have been tested with the aim of getting the TV viewer more involved. For example, Admeira’s “OK button” offers a convenient way for the viewer to interact with the televised content. When a spot is displayed, a prompt to press the OK button on the remote control appears at the bottom of the screen. This will open a page where recipes, videos or live statistics for sport events can be viewed. As a follow up, it is also possible to order brand products as a conversion target. The requirement for the up-front costs is that the viewer has previously agreed to use HbbTV, interactive advertising and watches the spots on live TV.

"Interactivity is a creative method that can be used to engender greater consumer interest in advertising and is a powerful instrument to ensure that TV advertising remains attractive in the future. Advertisers tend to be interested in interactive TV as an advertising format, which has resulted in increasing budgets for brand campaigns.”

The innovations must take place in a lean-back mode and need to be delivered to the consumer in form of high-quality, user-friendly content in order to achieve a consistently pleasing user experience. Content from the programmes should be offered to consumers through direct contact by means of the remote control.

Live and Sports events as very attractive advertising platform

Live sports become increasingly important in the TV Ad market. Fierce competition for exclusive broadcast rights has emerged. New pay-TV channels are spending huge amounts to win these precious rights to broadcast live sports. In addition, digital OTT platforms like DAZN compete for sport fans’ leisure time. The shift of sports content from ad-financed free television to pay-TV may result in a certain decline of advertising revenues from sports formats. Nonetheless, live and Sports events remain a key channel for advertisers to reach viewers through TV advertising.

"Live and sport events on TV continue to attract an incredible number of people. There are entertaining TV shows that fascinate a wide range of audiences and gather them in front of the TV. Simultaneously people discuss these events in the net. For such formats time-shifted consumption plays a negligible role which manifests that TV is still the best ROI-Media and the only mass medium.”

Merging media landscape

Foreign competition puts the Swiss media marketers under pressure in a battle for old and new markets. Media enterprises now consider it an imperative to own the user experience. In effort to achieve this, they are acquiring and integrating E&M assets at a faster pace and on a larger scale than ever before. According to PwC’s TMT Deals Insights, the number of global media and telecom deals rose by 29 per cent in 2017. This trend in M&A activities is also reflected in the Swiss media market.

In late 2017, one of the leaders in the Swiss advertising market, Goldbach Group AG, was integrated into Tamedia by means of a public takeover. With Tamedia’s more than 50 media and digital platforms, Neo Advertising’s OOH expertise and Goldbach’s leadership in marketing electronic media, the companies plan to offer a “360-degree offering” for television, radio, print and online media as well as OOH advertising.

Admeira, the joint venture founded in 2016 by Ringier, Swisscom and SRG, is looking to part ways with SRG. The joint venture was established to oppose growing international competition in the media advertisement sector. Ringier and Swisscom are each expected to take over 50% of SRG’s shares.

Taking Artificial Intelligence (AI) to the next level

AI is going to play a key role in the E&M market of the future. AI and machine learning are essential to improve advertising efficiency and effectiveness. With more sophisticated proprietary and third-party data, the use of AI is surely set to escalate. AI will reshape current TV planning in different areas, from realtime marketing, mix modelling to media buying. Thanks to the specific insights it offers, AI will allow advertisers to construct plans ad hoc, predict how ads will perform, and enable them to plan on both ratings and response. TV is in its next stage of evolution and the adoption of AI will help brands find the perfect place for TV advertising in their media mix.

Reaching the customer directly

Media companies have identified the need to have direct consumer relationships to stay relevant in the years to come. Two out of three consumers expect a direct brand connectivity. By directly addressing the viewer, companies collect data and thereby get to know the consumer. For example, TV advertisers using mini ads or interactive content allow stand-alone brands or companies in general to generate brand awareness and therefore help them with their marketing strategy. By delivering their message via television or alternative media, companies forego retail and seek a direct link to the customer.

New KPIs for TV

2018 will bring change to performance metrics for TV advertising. Common KPIs like GRPs, CPMs and ratings will still be important and widely used – especially for brand awareness – but we’ll witness more usage of brand-specific, performance-based metrics this year. Most sales directly due to TV are easily measurable by connecting the spot airing to an immediate action like an online sale, registration or subscription. Conversions in low-commitment products happen closer to spot airing than products with strong loyalty. For the latter, it is more difficult to tie a purchase directly to a TV spot. As a result, advertisers will turn to action- or intent-based metrics.

Shorter ads, bigger impact

Consumers are more receptive to short, skippable video ads. A US survey showed that over 44 per cent of all respondents answered that, next to skippable ads, short videos are a top factor for video ad receptiveness. The tendency towards shorter ads is also evident in the Swiss advertising market. As the Internet emerges as the new dominant platform for ads, traditional channels more often serve as promotion for owned media. For this reason, a brand’s story doesn’t have to be fully told on TV. Hence the move towards shorter formats and shorter spots. In 2017, ads under 10 seconds in length were televised 138,000 times more often than the previous year. The same trend applies to spots with a duration of 11 to 20 seconds, which outpaced the prior-year reading by a whopping 360,000. Spots in excess of 30 seconds are on the decline with a year-on-year reduction of 34,000. This trend underscores the shift to shorter but more specified content in advertising.

Live (sports) events, like the FIFA World Cup and the Olympic Games, remain a crucial factor for TV advertising revenues, as can be seen in the yearly fluctuations of the market. Like in previous years, the Swiss TV advertising market faces what at times are dramatic fluctuations in revenues due to high-grossing sports years, followed by years with a dearth of those big events. Live sport programming and the related cyclical boosts remain absolutely key for the segment. Regardless of these fluctuations, the non-digital TV advertising and sponsoring revenue streams are challenged by the digitalisation, hence our small projected growth of 0.1% CAGR for broadcast advertising and sponsoring. Mobile and online television advertising is continuing to show growth rates with a CAGR of 13.0% through 2022. On the whole, the TV advertising sector is expected to increase slightly by a mean reading of 0.4% (CAGR) over the next five years. Sponsoring will continue to fluctuate; sports years are unlikely to fully offset the general trend, therefore a decrease of -0.4% CAGR is expected.

According to the industry experts we surveyed, the Swiss TV market as a whole is considered stable for the coming years. We expect the total market to grow at a 0.4% CAGR. A slump like that seen in the print sector is not expected in the near future, even in consideration of the strong international competition from online OTT giants. Furthermore, online and mobile television advertising has been on the rise in recent years as a way of compensating for the uncertainties in broadcast advertising.

The Western European TV market should continue to grow gradually at an average annual rate of 2.0% through 2022. As the market is mature, television advertising growth will rely on the online and mobile segment which should record double-digit growth in many Western European countries.

After significantly adjusted predictions of total television advertising revenues, the UK will now only be the second largest player in Western Europe in 2022. With its CHF 5.9 billion in revenues, Germany is expected to take the lead. In absolute numbers, the Swiss market generates less than the Netherlands but more than Sweden.

Switzerland, a saturated TV market, faces various challenges such as changing consumer expectations, alternative entertainment sources or the trend towards digital content consumption. Traditional TV stations in Western Europe face the same challenges as providers in Switzerland and need to adapt to a globalised, highly competitive environment. Big private TV stations, banking on pay-TV and appealing live-sport packages, will expand across Europe and compete for local market shares. In addition, alternative content providers like OTT platforms are fighting for the customer’s valuable leisure time, making it only harder for TV stations to lure people in front of the screen.

{{item.text}}

{{item.text}}

Bogdan Sutter

Director Advisory, Strategy und Transformation Expert, PwC Switzerland

Tel: +41 79 356 30 80