Sports industry: system rebooting

PwC’s Sports Survey 2020

In this particularly turbulent time for our sector marked by COVID-19, we’re pleased to have gathered the views of 780 industry leaders coming from 50 countries – a record number of respondents for the second year in a row.

As expected, the fifth edition of the PwC’s Sports Survey closely reviews the short- and long-term consequences of a crisis unprecedented in the history of modern sport. Against this backdrop, we’ve delved into the rapidly evolving sports media ecosystem, as well as the opportunities and challenges of emancipating esports as a new discipline alongside its physical equivalent.

The state of the sports industry

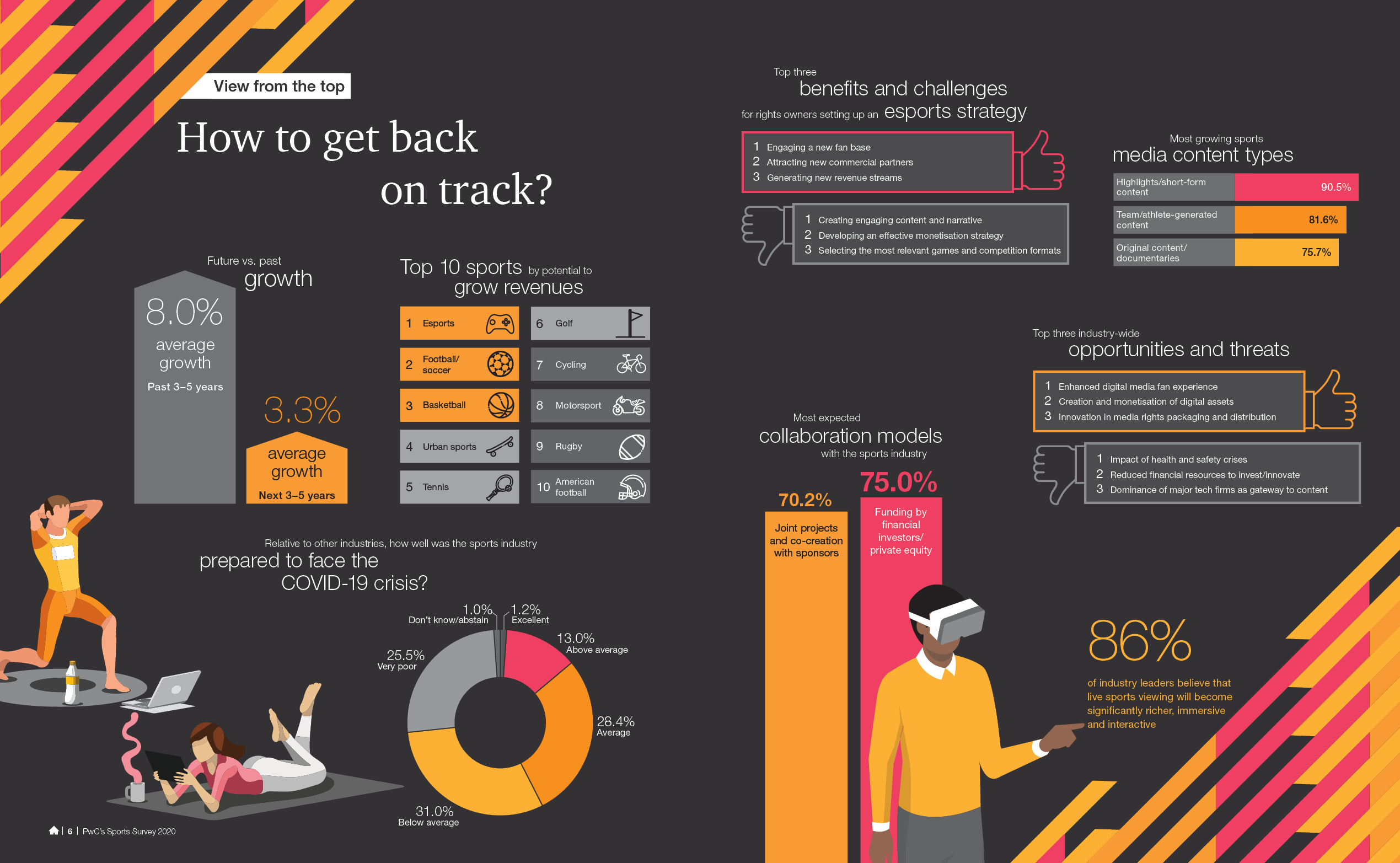

Each year, we survey a select group of industry leaders on their perceptions of the growth, key opportunities and threats faced by the sports market. Through this exercise, we aim to provide you with macro insights on how our industry is likely to develop in the coming three to five years. This section outlines high level takeaways, setting the stage for the following chapters which address in greater detail the impact of COVID-19, the market dynamics reshaping sports media as well as the growing opportunities in esports.

In general, our results show that the prevailing pessimism is cut by the many opportunities brought about by the crisis. This situation may favour the emergence of changes that have long been considered but never achieved to their full extent, whether it be hybrid sports, new revenue streams, drastic governance reforms or enhanced collaborative models.

Explore this year's insights

Impact of COVID-19: winds of change

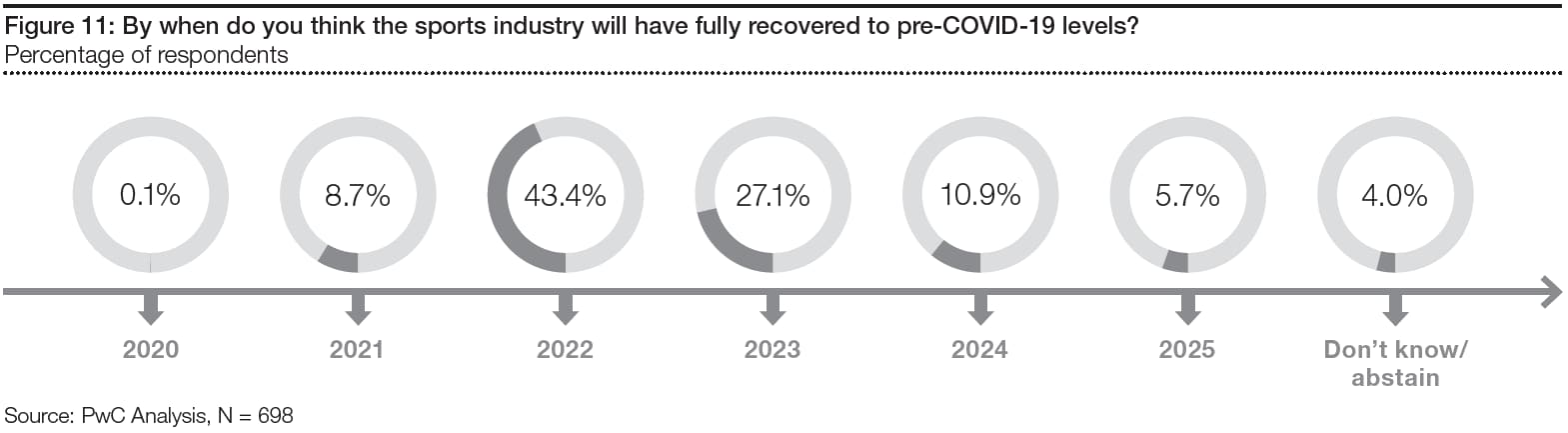

The sports industry was far from being prepared to absorb a shock of this magnitude, shattering the false sense of security on which it had been relying for years. The entire sector has been affected, from grassroots to elite, with fundamentally harmful effects on properties that are highly dependent on physical manifestations.

Beyond the structural risks inherent in the industry’s natural ties with crowds and events, the crisis also brought systemic weaknesses to the surface, suggesting prospects for profound change. Indeed, the then-weak signals related to shifting consumption behaviours, mutation of revenue models, as well as the arrival of external investors have now become tangible trends. It’s vital that sports organisations fully address these issues with the perspective of turning them into opportunities.

All in all, the underlying challenges only shed light on the importance of innovation, proactivism and cooperation to protect and support the growth of the industry over the medium- and long-term. With regard to collaboration, we foresee the end of the historical, in-house vs. outsourcing binary model in favour of more symmetrical schemes, driven by value cocreation and shared accountability of results

Sports media: navigating the age of complexity

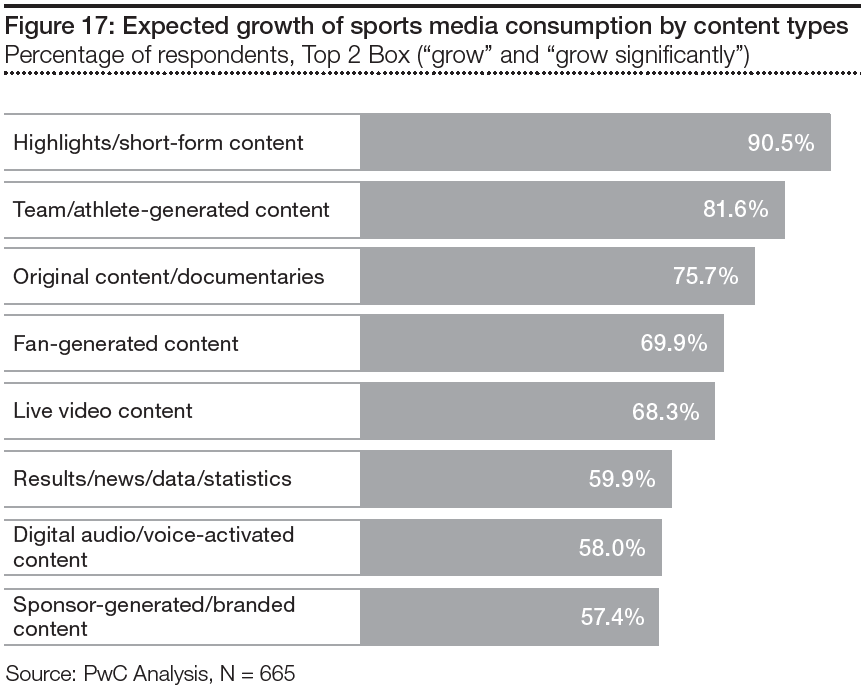

Historically, the industry has drawn its commercial value from live sports. The COVID-19 shock has weakened this, fostering the adoption of alternative content formats. This new pattern pushes sports properties towards shaping their content strategies beyond events, paving the way for omnichannel and multiplatform storytelling.

The acceleration in cord-cutting, piracy and audience fragmentation are putting tangible pressure on the value of sizable, exclusive media rights deals. This underlying threat raises important questions on how rights owners should approach exclusivity. We predict the near-term adoption of more diversified content distribution models, shaping a liquid market.

Augmenting the fan experience might be on everyone’s lips, but sports-related digital platforms haven’t cracked it yet. As immersive solutions go mainstream in line with technological progress, consumption preferences need to be understood with higher granularity to enable the enable the design and implementation of features that meet their needs.

In the broad scheme of things, the dynamics of the sports media market are becoming more complex. As sports are being consumed in a pluralistic way, marking the end of the historical monopoly of the live format, the proliferation of content buyers is contributing towards forming an ecosystem that is increasingly difficult for content distributors to control. This is the dawn of a new, convoluted reality in a market once simplified by the dominance of TV giants.

Esports: the great emancipation

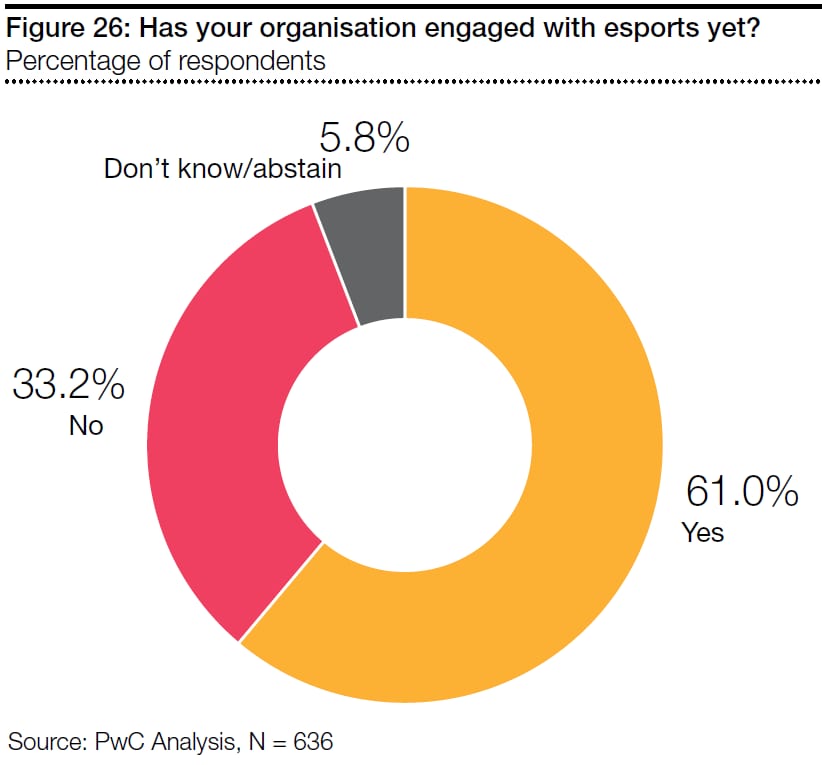

Generally speaking, it is clear that the COVID-19 crisis has favoured the acceleration of virtual entertainment, improving the odds for simulated sports esports. While our analysis shows that the underlying trend is likely to continue over the long term, it should nevertheless not be taken for granted. Sports organisations need to carry full responsibility for their esports strategy and ride the wave before other games win and lock in consumers.

The central insight from our survey is the importance for rights owners to stop considering esports merely as a fan engagement tool but as a genuine discipline with its own rules, fans, heroes, and culture. Developing such a model is similar to developing a new product or a brand; it can only be part of a long-term process. The advent of hybrid sports – which puts an end to the perennial debate about the physical aspect of esports – has now reinforced both the legitimacy and potential of virtual sports within federations’ discipline portfolios.

Reflecting on the trends impacting the media market for traditional sports, rights owners must be inclined to experiment and diversify, with the vision of building their very own revenue ecosystem. If simulated sports esports does not yet have a dominant financing model, the wide variety and speed of the market imply that this may never be the case. For this very reason, the sports industry must be bold enough to break down boundaries and dogmas in order to truly emancipate itself both creatively and financially. This, to us, is the only path to esports success.

Download the survey

https://pages.pwc.ch/core-asset-page?asset_id=7014L0000000jkZQAQ&lang=en&embed=true

Contact us